SMM February 21 News:

As of February 21, domestic zinc concentrate TCs rose to 2,750 yuan/mt (metal content), and imported zinc concentrate TCs increased to $20/dmt. Since the beginning of 2025, domestic and imported zinc concentrate TCs have risen by 900 yuan/mt (metal content) and $40/dmt, respectively, with the growth rate significantly faster than in H2 last year. Can this upward trend be sustained? How will TCs evolve in the future?

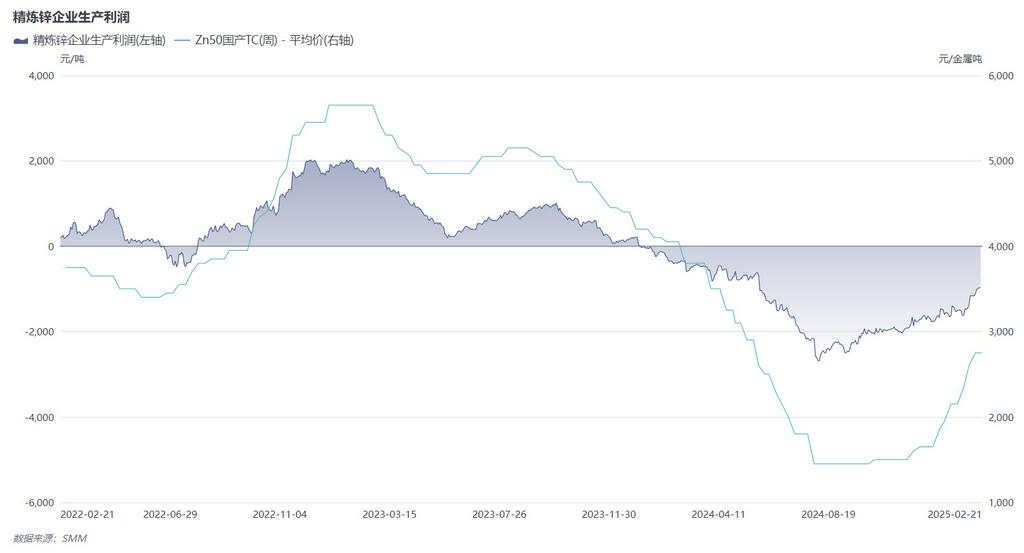

From the perspective of smelter profits, although both domestic and imported ore TCs continue to rise, based on current zinc prices and TC levels, smelters' profits excluding sulphuric acid and by-products are still in deficit by about 1,000 yuan/mt (metal content). Most smelters with average comprehensive recovery capabilities remain slightly unprofitable. Therefore, in the short term, smelters are maintaining a strong sentiment to stand firm on quotes for subsequent TCs to achieve profitability as soon as possible.

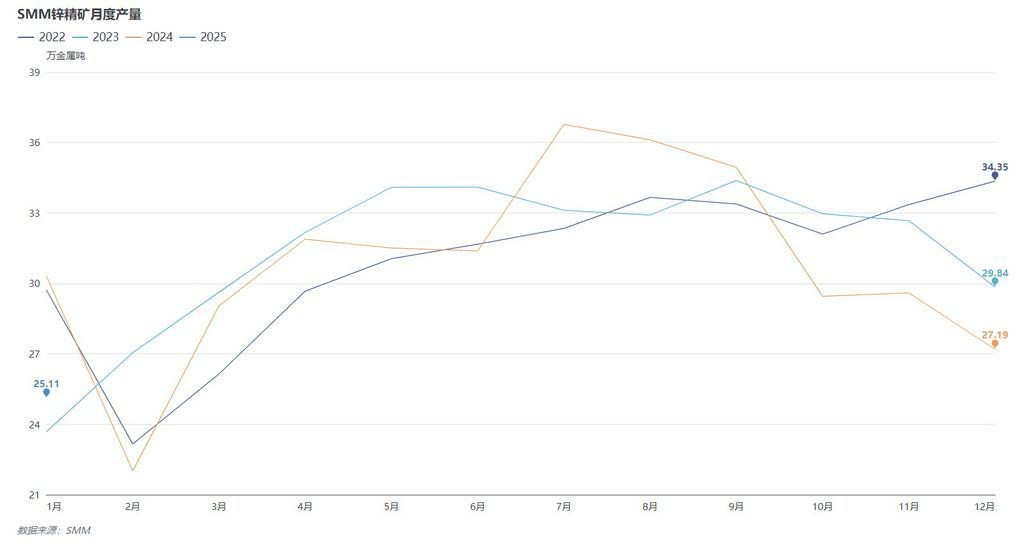

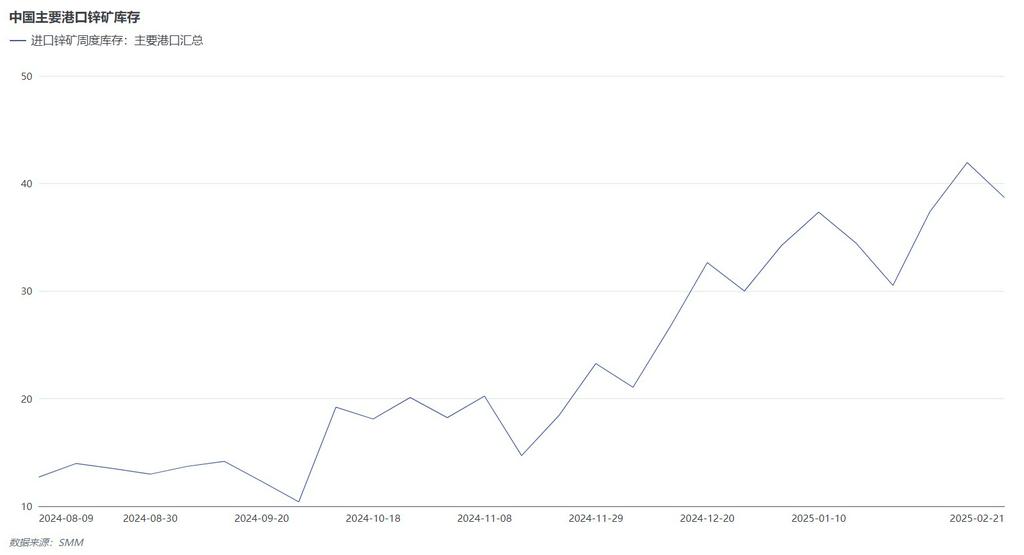

In terms of supply, the year-end and beginning of the year are traditional shutdown seasons for some mines in northern China, with shutdown durations ranging from 2 to 4 months. These mines are expected to gradually resume production starting in March and fully recover by June. Thus, domestic zinc ore supply is expected to see continuous MoM growth in the coming months. Regarding imported ore, although January's domestic imported zinc ore data has not yet been released, since the beginning of the year, zinc ore inventory at Chinese ports has remained above 300,000 mt, providing sustained supply support for the domestic market.

From the demand perspective, early February coincided with the Chinese New Year holiday, coupled with fewer production days in the calendar month. SMM expects domestic refined zinc production in February to experience a seasonal decline, with some plants reducing raw material procurement volumes, further driving up domestic and imported TCs. Meanwhile, as domestic smelters have not yet fully achieved profitability, significant production increases are unlikely in the short term, and the demand side is expected to remain stable.

Overall, domestic negotiations for March zinc concentrate TCs are set to begin next week, with smelters maintaining a strong sentiment to stand firm on quotes. Domestic and imported TCs are expected to continue rising. However, in the long term, as domestic smelters gradually achieve profitability, Yunnan Copper, Wanyang, and some previously suspended small plants are expected to resume and ramp up production, significantly boosting zinc ore demand. At the same time, the market also anticipates an increase in overseas zinc ore supply. With both supply and demand increasing, SMM will continue to monitor the subsequent TC trends.

》View SMM Metal Industry Chain Database